I’ve been too positive about the entertainment industry recently. Especially the traditional players. I think theaters by the end of 2021 will be fine. I think the traditional entertainment streamers can compete with Netflix (and Amazon). And I even think Disney will see a thriving theme park business sooner rather than later.

So let’s get negative. Really inspire some fear. Of course, that means broadcast TV.

(As always, if you’d like the Entertainment Strategy Guy delivered to your inbox, sign up over at Substack. My newsletter is free and goes out every two weeks.)

Most Important Story of the Week – TV Network Ad-Revenue is at Risk

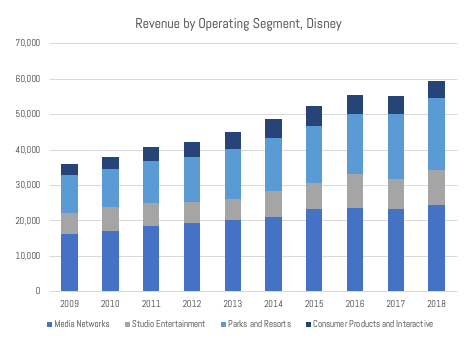

While it may be “dying”, the linear TV business is still good money for traditional media conglomerates (Disney, Comcast/NBCU, AT&T/Warner Media). I like to tell this story via this chart via Disney’s revenue:

In addition to the total revenue, media networks also make tons of operating profit. As I laid out in one of my most popular articles of the year, if you imagine a world where, in complete disruption, they lose all their “media networks” operating profit, and streaming still isn’t profitable, they aren’t just losing $3 billion per year like Netflix, they’d have lost $10.5 billion in operating profit on net!

Thus, as they pivot from linear to streaming, the traditional players need to be careful. They need to find out how to make streaming profitable and not destroy their cash cows that quickly. It’s unclear if anyone can do the former, and the Coronavirus may have pushed the latter from their control.

Advertising revenue will be the first part of the traditional linear pie to feel the pain. (And actually has been suffering in the last few years.) It’s not a majority of the revenue–that honor belongs to subscriber fees–but it’s a big portion of the puzzle. Across broadcast and cable, it’s a $44 billion dollar piece! Depending on the channel, it can be 20-50% of total revenue.

And the biggest piece of advertising revenue comes from the broadcasters, which are still the biggest channels in the linear bundle. The threats to advertising come from both the demand and supply sides, which is what makes the Covid-19 inspired recession particularly challenging. (Past articles on Covid-19’s impact on entertainment here, here, here, here or here.)

On the demand side, advertisers love to advertise on sports because live sports still get great ratings and viewers don’t usually skip the ads. And when I say sports, I mean football. Both college and NFL, but particularly the NFL, which dominates annual ratings. While the NFL is still scheduled for this season, it could disappear in a moment’s notice if Covid-19 rates skyrocket again. Thus, the Wall Street Journal reports that advertisers are seeking to claw back proposed ad spending if NFL games don’t happen.

(As for college football, a majority of college football games have been cancelled, but some leagues–the SEC, Big 12 and ACC–are trying anyways.)

If the broadcast networks lose NFL games, it’s doubly-brutal since the rest of their primetime schedule is fairly “meh”. The same force that could cancel NFL games caused studios to shut down all of production for new TV shows. Reruns don’t do as well as new TV shows. Thus, the linear channels will have fairly weak lineups this fall, even as customers have more free time than ever to watch.

There is one bright spot in the demand-side: out-of-home viewership. For years Nielsen didn’t mention viewership in bars or restaurants or anywhere that wasn’t in someone’s home. But obviously sports bars only exist to show sports and serve beer. After years of promise, and some last minute waffling, Nielsen plans to roll this out this fall. It should boost the role of sports/ESPN even further in the ratings. (And 24/7 news networks.) That said, if the NFL doesn’t happen, no amount of out-of-home viewing will help.

The supply side of ads is arguably in an even worse state than the demand. When you’re in a recession, the first thing that goes is marketing expenses, and that’s precisely what happened in this recession. Some of the biggest drivers of ads are under as much threat as the broadcasters, like car companies, airlines, or hotels. And they’ve pulled back on advertising. Meanwhile, digital advertising beckons with its “targeted” ads, since Google, Apple, Amazon and Facebook hoover up all your data to sell.

And one of the biggest advertisers, Hollywood itself, will probably spend the least on linear advertising in recent memory. Since, theaters have been shuttered in large parts of the country, there is no big opening weekend to push customers towards. Digital advertising can take up that slack. That’s the take in this Variety story.

Conclusions

That’s the doom and gloom for the near term. Will it last?

Again, when everything is tied to Covid-19, there is as much a chance that things snap mostly back when the pandemic passes as it is that they are permanently altered. (For the record, I expected/will expect double digit drops in linear viewership since cord-cutting adoption is following an S-curve.) For example, if theaters are back to “normal” in the mid-point of 2021, the focus on opening weekends will return, and with it linear advertising.

If I had to point to one wildcard, though, it’s football. Which is really the issue suffusing the conversation above. (Even feature films are really talking about advertising against football.) As long as football wants to reach every household in America, it needs linear TV as much as digital. And that should support this ecosystem for another 5-10 years.

Still, we’ve likely seen a high watermark in linear advertising revenue. Which isn’t too surprising, since advertising revenue has been under pressure for years. It just means that, even if it bounces back, between cord cutting and reduced quality content, broadcast advertising will never regain its past heights.

Entertainment Strategy Guy Story Updates – Licensing Is Still Very Important for Streamers

This story is really a combination of three stories that all competed for my top slot this week.

- First, Lucas Shaw digs into the negotiations/bidding for the “Pay 1” rights for Universal, Sony and (maybe) Paramount’s movies.

- Second, Nielsen released their first batch of “streaming TV” ratings in America. (For televisions only, which is a key caveat, but if this feature goes forward this will be a great source of data.)

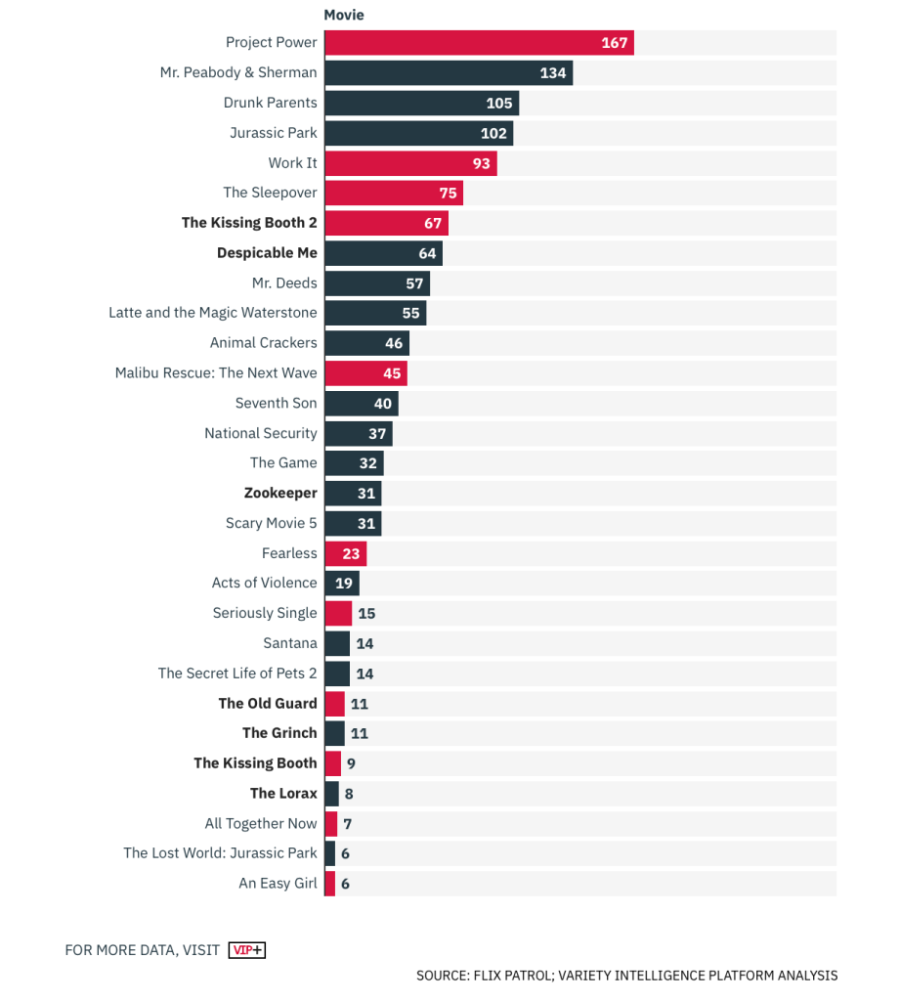

- Third, Variety VIP is partnering with FlixPatrol to release monthly ratings based on Netflix top ten lists globally.

Combine the three and the story is fairly inescapable: for all their tens of billions in content spend each year, Netflix cannot give up on licensed content. This shouldn’t be that surprising, but it does contradict the story Netflix projects to Wall Street.

Let’s start with why licensing is still crucial: because it moves the needle! When you look at the Pay-1 movies–films in their first linear TV or streaming window after theaters, usually in the first year–you can see that every streamer is desperate to get Universal’s output. This is because new Fast and the Furious, Minions, and Jurassic Park films move the subscriber needle. Just take a gander at VIP’s August report:

(Go to Variety VIP to read. Full disclosure: I’m on a free trial from Variety.)

That’s a lot of licensed film content in Netflix’s Top Ten! The story is the same on Nielsen (hat tip Alex Zalben) when it comes to top TV series on Netflix in the last week:

That top ten list is almost all licensed content. (Which contradicts Netflix’s daily Top Ten lists, a point I’ll explore in a future article/Tweets.)

On the whole, the fact that Netflix needs licensed content should be the least surprising story in media. TV has always been about renting content. Syndication built up numerous channels from Fox to USA to AMC to you name it. Even HBO was built off Pay 1 films. So renting content to enter a market is a tried and true strategy..

Unless…

…your stock price involves “building a moat” of original content. Which Netflix’s does. Specifically, making a moat with original content that will bring “pricing power”.

Licensed content’s current and continuing importance to Netflix will determine if this strategy works or blows up. If it turns out that Netflix still needs licensed content, after spending billions on originals, then one of two things happen. First, if Netflix loses the content, then they will likely see higher churn among customers. That both lowers the average revenue per user and raises acquisition costs. So they keep losing money. Or Netflix keeps licensed content, but has to pay more and more for it in a competitive bidding environment. That raises their costs. So they keep losing money.

In short, Netflix desperately wants to decrease its reliance on licensed content. But so far the data doesn’t show that strategy is working.

Over the last few months, I’ve softened on how important licensed content was for Netflix. It seemed like their original films were finally breaking through. And the top ten lists were filled with originals, especially on TV. But the combined FlixPatrol/Nielsen data contradicts that. Even as the licensed content changes–farewell Friends, The Office, and Disney blockbusters–the importance of licensed content remains. (My guess is Hulu and Prime Video are in the exact same boat, by the way.)

(Bonus update: it seems increasingly clear that the future will be measured, as I wrote way back in December of 2018 and October of 2019. Between top ten lists, Nielsen and others, we’ll have some sort of standard to judge which shows are doing well in the ratings.)

Other ESG Update: Cobra Kai’s Migration to Netflix

To quote Marshall McCluhan, the medium is the message. So for Youtube, the medium is ad-supported music videos, box openings and alt-right/alt-left commentariat. Not prestige originals. Clearly Youtube had a good show in Cobra Kai, but after that they didn’t know what to do with it. (Read my past writings on Youtube Originals for more.)

Other Contenders for Most Important Story

AT&T Is Selling Some Assets, but Not Others

The story over the last few weeks has been that AT&T is looking to sell tertiary businesses to reduce debt. On the table are Xandr (their ad-sales unit), DirecTV and CrunchyRoll; not on the table are Warner Media’s video game unit. As some folks have pointed out, though, we shouldn’t read too much into any specific business unit sale or story since these talks are ongoing. And the rumor mill is vicious.

Still, it seems clear based on the volume of rumors that AT&T is looking to sell some assets to help their balance sheet. The management lesson should be clear: M&A is not a strategy. Strategy is strategy. That’s the story of AT&T in the 2010s: buying size mostly to accumulate assets. The investment bankers got paid; the shareholders haven’t yet.

Walmart’s New Subscription

On the surface, Walmart offering “Walmart+” isn’t entertainment related. It’s an ecommerce story, about a battle between two monopolistic giants. Except for the fact that nearly every article had to mention that Walmart+ doesn’t offer any free entertainment streaming. So…

Prime Video = $120 a year, with Prime video and Prime Music

Walmart+ = $98, with no entertainment.

Therefore, Prime Video and Prime Music are worth $22 a year?

Listen, that math isn’t totally correct. There are tons of unaccounted for variables. But generally does it match consumer demand? It probably isn’t that far off either.

Data of the Week – What is the U.S. Addressable Market for Streaming?

In a lot of ways, isn’t that the question of the streaming wars?

A few weeks back, Leichtman Research group updated their estimate for the number of broadband homes in America. In 2019, America reached 101 million broadband homes. On the bass diffusion curve, clearly broadband adoption is slowing. This could be a good proxy for cord-cutting homes, since if you don’t have broadband you can’t stream.

Meanwhile, Nielsen still counts about 121 million homes as “TV watching” homes. Meaning about 20 million homes are still cut off from cord cutting in general.

So, the natural question is do Netflix, Hulu, Prime Video, HBO Max and Disney+ all have aspiration of 100 million household penetration in the future? Probably not. As my past research has shown, Netflix will likely tap out at around 70 million US subscribers. Meaning we have a gap of about 30 million households.

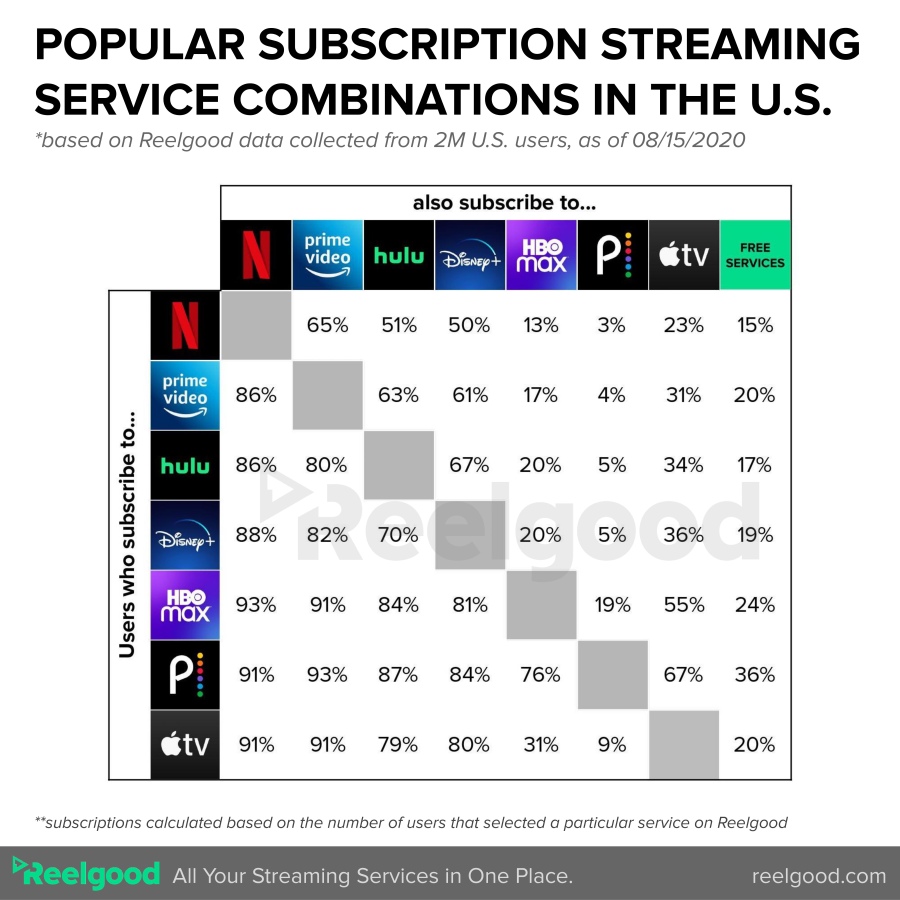

While overall streaming could end up reaching 100 million homes–similar to cable at its peak–there won’t be one service that every household subscribes to. Either from keeping skinny bundles, sharing passwords or what not, I don’t think we end up with one service as the “universally owned” streamer. This data from Reelgood shows that while Netflix is the closest to a universal streamer, many streamers have bundles which don’t include it.

And if Netfllix can’t do it, I don’t see anyone else doing it either.

Lots of News with No News

Another Netflix Producing Deal

With royalty no less. Or not, since I believe they renounced their titles? Listen, I’m not an expert on British nobility. And while I can understand the interest from a general entertainment perspective, from a business standpoint this doesn’t move the needle.

Sound Issues in Tenet

Since Tenet isn’t in theaters in the U.S., and won’t be in my neighborhood anytime soon, I can’t speak to this from first hand information. But apparently customers are having trouble hearing crucial pieces of dialogue in Tenet. That said, when it comes to most TV and films it can be hard to hear many of the lines. Sound mixing has a lot of trouble dealing with everyone’s different sound systems nowadays.