We have a special treat today…an interview with Matt Strauss, head of Peacock’s launch.

Kidding!

I guess I’m the one entertainment outlet that didn’t get that interview. (Seriously, how many interviews did he do over the last month or so?) Like America in World War II, our last entrant joins the streaming wars and that’s our story of the week.

(As a reminder, if you want to connect on social media, try me on Twitter or Linked-In.)

Most Important Story of the Week – Peacock Launches!!!

The last entrant of a major streamer has landed for American distribution. Comcast’s NBC Universal’s streaming platform launched on Wednesday. In full-disclosure, I haven’t used it yet.

(Why? Because I find most “reviews” of UX/UI aren’t objective measures of quality but subjective repetition of preexisting positions. If you thought Peacock would be a bust at launch, you’ll likely hate it. If you’re bullish on traditional entertainment companies–like me–you’ll likely find positive elements.)

From what I hear, the service announced in January is the service we’ve gotten. Strategically, I think Peacock is a pretty smart play by Comcast. First, it’s free, which means it’s competing on price. Second, it’s a FAST on steroids, meaning it’s got a lineup that IMDb TV and Roku Channels (and Tumo/Xumi) can’t match. Third, live sports and news are differentiators. I summarized this is in a thread:

1/ Happy Peacock Day! Hopefully a tradition we can celebrate for years to come. In honor, a thread:

My strategic optimism for Peacock on launch day.

— The Entertainment Strategy Guy (@EntStrategyGuy) July 15, 2020

(For my longer-ish take, go back to January after their announcement.)

Instead of their strategy, then, let’s explore how Peacock really is the synthesis of many ideas impacting the streaming wars. (Many of which I’ve written about previously.)

Device/Distribution Wars are the Nu-Carriage Wars

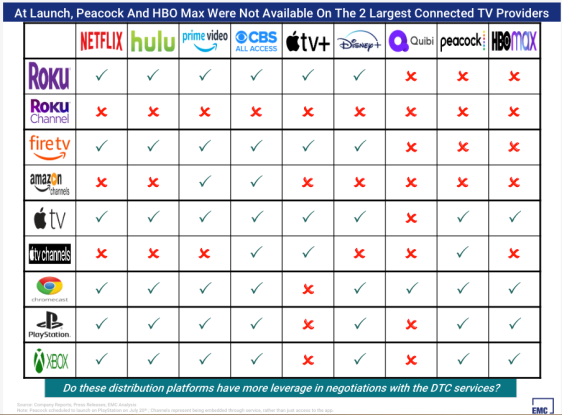

Another streaming service, another holdout by Amazon and Roku against offering the app as a standalone on their devices. Last summer, all the news was about MVPD retransmission battles, such that it made my story of the week in July. But already, I could see the future battleground moving from retransmission to devices. (The Apple/Amazon distribution fight was particularly fierce, if not widely covered.) EMC Capital provided a good summary chart of the landscape:

(This is one of those simple charts that I’m jealous I didn’t make myself. Click here to subscribe to EMC’s newsletter.)

It seems that the traditional entertainment companies have finally realized how valuable owning the customer relationship (and data) is for direct-to-consumer businesses. The challenge is that the device owners (Roku, Amazon, Apple and maybe Google) are in a better position. Because they control the user experience and potentially billing, they can offer better bundles and experience. More importantly, the key applications (Netflix, Prime Video, and Hulu) take the bulk of customer’s time, so as long as a device has those, it’s likely won’t offend customers by not having the newly launched entrants (not named Disney+).

As I wrote in June, it is in the interests of HBO Max and Peacock to hold out as long as possible. Amazon’s user experience has always been sub-par, and it devalues their content to be mixed in with who knows what content is on Prime Video. (Seriously, Amazon just added profiles to their interface…) Meanwhile, it’s one thing to pay a fee to be on a service; it’s another to let Roku or Amazon own the customer relationship. Or to take the bulk of your ad-inventory.

Can the dual absences of HBO Max and Peacock hurt Roku or Fire TV sales? That’s unclear. Clearly Amazon and Roku looked at Disney+ and saw an app they couldn’t say no to. But that set a precedent HBO Max and Peacock will cling to.

Part of me thinks this will help Apple TV devices, but only for new customers. I myself may be purchasing a new streaming device this fall; the clear winner for me is Apple TV or X-Box since they have every service I want. (I’m not convinced I need Apple TV+ just yet.)

Comcast Is Powering It’s Flywheel

I kid! Obviously, I think flywheels are an overused concept in streaming video. And tech period. (See my two very, very long articles explaining this here and here.)

One can’t discuss Comcast’s business model without seeing the similarities to Apple or Amazon. Comcast is launching a potential Deficit-Financed Business Unit (DFBUs) in Peacock to increase revenue in another line of business, cable internet. They are bringing folks into their “cable ecosystem” via deficits because they offer Peacock’s $5 plan for free to existing Comcast and Cox subscribers. If you think it’s a good idea for Amazon to sell Prime Video at a loss to drive Prime memberships or Apple to offer Apple TV+ to sell more iPhones (both DFBUs into ecosystems), then you should be fine with Comcast selling streaming at a loss to keep cable subscribers.

The difference? Apple and Amazon are supported by tech valuations, and Comcast has a lowly cable company valuation. That and my next point.

Comcast Really Does Everything in Digital Media

Now that Comcast has their ad-supported and subscription-supported service, to add to Vudu/Fandango’s TVOD business, and NBC’s broadcast business and Bravo/USA Network/et al’s cable business, and Universal’s movie business, man, Comcast does have it all!

I hold to my thesis from a few months back: Comcast wants to pivot into partially being a tech company. Hence the push to have a holistic digital offering very similar to Apple or Amazon. This will hopefully supplement and/or replace their declining cable and satellite businesses.

Of course, you can see the clash with the “flywheel” thought above. Whereas Apple and Amazon can afford to lose lots of money–though affording to does not mean they should–Comcast doesn’t have that luxury. Further, for anyone not in Comcast’s cable footprint, there is no ecosystem to bring customers into. Like Disney and AT&T, Comcast needs to make money in streaming.

One Thing to Watch: The Churn Hypothesis

A big theory of Netflix bears–those pessimistic on its stock price–is NOT that Netflix will die. There is no way that suddenly 63 million US subscribers abandon the service. That’s not the argument.

Instead, the argument is that with digital subscriptions the name of the game is “churn”. The number of folks leaving a service versus the number joining.

Historically, Netflix has had astoundingly low churn. Some have estimated it at 3% per month, though I’ve speculated it’s higher. Since Disney+ launched, we’ve seen evidence that churn is up. And while the data is super noisy–and part of the “asterisk extraordinaire” coronavirus times–that churn has picked up during Covid-19.

This has matched a thesis I’ve supported, but discovered through conversations with Hedgeye’s Andrew Freedman and Twitterzen MasaSonCapital. The thesis isn’t that anyone will “kill” Netflix. Instead, the launch of new streamers powered by the three best studios for content (Disney, then Warner Bros, then NBC-Universal) will make life more expensive for Netflix. That will show up in churn.

Between HBO Max and Peacock, I think there are bundles that are increasingly viable that don’t have Netflix in them. Obviously, this isn’t for everyone! Some folks will always have Netflix. But other folks will start to use Netflix in chunks watching for a period, disconnecting and coming back.

Either way, this is what I’m watching as Peacock launches and all the streamers begin to compete.

Entertainment Strategy Guy Update – Apple’s Services Business Model Weaknesses

Over the last month or so, Apple’s seen a string of bad news stories that add up to a trend. That trend being that they aren’t very good at launching entertainment subscription services.

– Apple Arcade is cancelling some development deals.

– Apple News lost The New York Times (and previously had underwhelming numbers)

– No news is bad news for Apple TV+.

– Apple got into a fight with app developers over fees. Regulators may step in.

Yet, after last quarter’s earnings report, Apple reported all-time highs in services-related revenue. So clearly, something must be working?

I don’t think so. Instead, I think the non-entertainment subscriptions are the engine driving the Apple car. My gut is that Apple Care is the bulk of the subscription revenue followed by fees charged for the app store. Then it’s followed by Apple Music, which is the one entertainment service that had the best chance since everyone with an iPhone used iTunes for music. (And many fewer used it for TV.)

I wish I had better data to estimate the service revenue for Apple more precisely, but that’s a bit too time consuming for a weekly column. It’s worth noting that if the bulk of services revenue comes from insurance and then fees to apps, it really doesn’t justify the push into entertainment services. Who loves insurance companies after all? This is a story to monitor.

Other Contenders for Most Important Story

Like most weeks, we’re running long. Let’s go quickly.

Nielsen Plans to Change Measurements

For years, Nielsen has wanted to track out-of-home viewing in the United States. To better capture TV ratings. (The hosts of ESPN’s sports talk show PTI, for example, claim they’d be the most watched show on TV if you included bars airing their program.) Executives have clamored for this too, and Nielsen was finally going to do it, then reversed course, presumably because of Covid-19. Then, under an onslaught of bad opinions, they reversed their reverse course.

End point? Out-of-home ratings will come this fall.

My concern is that this bump in ratings will be compared to past non-out-of-home numbers leading to endlessly confusing apples-to-hammers comparisons. Sigh. Still it will be more accurate, which is a good thing.

Peter Faricy Leaving Discovery

Multiple folks covered this story or sent me this article. So clearly folks consider this a big change.

On one hand, I acknowledge the focus on customers at both Amazon and Hulu. (In a previous The Information story, Jason Kilar said his job was to pivot AT&T to focus on customers.) It really is useful to focus on customers and it’s one of the things I admire about Amazon. That said we can take it too far, as this blog post hilariously debunks.

I’d add another crucial distinction: It may not be that Faricy was focused on customers, but that he’d never learned the discipline of staying on budget at Amazon.

When The Information writes about getting “a bit of Amazon’s magic”, they should include cash flow in that “magic”.

That’s the challenge of starting your career at Amazon but heading elsewhere: the entire business model is powered by cash flow from Amazon Web Services. It’s really easy to be “customer-focused” when you can lose $1 billion a year. It also helps that Amazon starts dozens of copy-cat and knock-off businesses every year and just shutters them if they don’t work. Again, it’s great to have tons of cash and a Wall Street that doesn’t ask too many questions.

I’ve been skeptical about Food Network Kitchen since it started. If Faricy thought that he’d be able to sell tons of additional appliances, gadgets and food delivery through a TV service, then he doesn’t know much about TV, frankly. I built a back of the envelope calculation showing how hard this would be. Faricy (and his allies who talked to The Information) can blame it on not being customer-centric, but they made a lot of bad decisions. They had a pie-in-the-sky plan based on dreamland economics. At Amazon, they can afford to take those risks; at Discovery they can’t.

Unlike Amazon, Discovery can’t just shutter Food Network Kitchen and move on. This business has to work. Hence, a culture clash.

Hobbit No Longer on HBO Max

Here’s some breaking news: The Hobbit movies from Warner Bros are no longer on HBO Max. They were there at launch–to much fanfare–but have since departed the service–to no fanfare. The moral of the story is to be careful who you license your content to. You may not be able to get it back.

Netflix Earnings

Overall, a good quarter verging on great, caveated with the “asterisk extraordinaire”. That being this is the Covid-19 full-quarter and at the end they saw some decline in users, which they attribute to dropping inactive accounts. The worry is this is the high water mark of free cash flow and subscriber growth (though not subscribers). We’ll see.

(I’m working on updating my charts on subscriber numbers since I haven’t done that in a pinch, but it won’t be ready until next week.)

M&A Updates – Sirius Buys Stitcher

The podcast consolidation wars are heating up. The biggest story is that Sirius XM bought podcast application Stitcher, to pair with the earlier purchase of Pandora. Like Comcast, Sirius sees the future in satellite audio as much weaker than the future in digital audio. Like Spotify, it also sees better margins in podcasting than music. (Frankly, it surprises me they didn’t go after Joe Rogan to pair with Howard Stern.)