Since May kicked off, I’ve been back to writing two articles per week and have had my highest traffic month since launch. So thank you to all the readers and supporters. If you want to stay on top of all my writings, the best method is to either subscribe to my newsletter (at Substack) or through the WordPress application.

Meanwhile, onto one of the more fascinating stories of the year…

Most Important Story of the Week – HBO Max and Amazon Stare Down

Well, HBO Max launched.

If you’re comparing hype, it feels way less substantial than Disney+. Or even Apple TV+. But that’s to be expected. Disney+ was a brand new thing by one of the most powerful brands in America; HBO Max is a retread of a brand most people already know. Meanwhile, while Warner Bros has always had big films and series, but they aren’t associated with their parent company.

Since the HBO Max that launched this week is mostly the service promised last fall, I’m going to focus on the issue we’re all obsessed with:

HBO Max didn’t launch on Amazon’s devices.

Technically, Roku devices too. But Amazon is the fascinating topic to me, since their negotiating position isn’t just about devices, it’s also about operating systems, content rights, and profit sharing. Let’s try to explain why this negotiating is too contentious, and so critical for AT&T to get right.

The Issue: Operating System vs Device

The core issue of the streaming wars is who gets to aggregate content and who gets to bundle that aggregated content. The aggregators are the streamers, in this case. Think Disney+. HBO Max. Netflix. Prime Video. Previously, they were the linear channels. And formerly ESPN, Disney Channel and HBO.

Bundlers figure out a way to offer access to streamers. In some cases, this is via device. Fire TV. Roku. Apple TV. Sometimes this is via an operating system. Like Apple Channels and Prime Video Channels. Maybe Hulu and Youtube in the future. Formerly, this was the MVPDs like Comcast, DirecTV and Spectrum.

Notice that Amazon has both a device and an operating system.

The trouble is their operating system is a lot like their streaming service. Specifically, if you subscribe to HBO through Prime Video channels, you can access your content via the Prime Video application. This way a customer using Amazon Channels can seamlessly go from Prime Video shows like The Marvelous Mrs. Maisel to Game of Thrones and The Sopranos. Honestly, you couldn’t tell the difference between where the content comes from.

From Amazon’s perspective, if HBO is already included in channels, then so should HBO Max. They signed a deal several years back to make this happen, so why not continue since every other HBO customer (mostly) gets HBO Max with HBO?

Because AT&T learned enough over the last few years to know what matters when launching a streamer. When HBO was mostly a cash play, Amazon was found money. Since HBO was also a key piece to Amazon Channels–clearly their biggest seller– Warner Bro negotiated fairly beneficial deal terms. The partnership worked, as Amazon felt free to leak that 5 million folks subscribe to HBO through their Channels program.

The difference between distributing on Fire TV devices and within Amazon Channels–and the fact that Amazon bundled those discussions together–basically shows how much AT&T stands to lose.

The Key Negotiating Deal Points

- User Experience – This issue more than any is what AT&T wants to control. Prime Video has been around for years, and it still gets the most “blah” reviews as a streaming platform. When AT&T sends its content to Prime Video–as it has to for the Channels program–it essentially gives up control for how it will be branded and leveraged. Try as you might to negotiate this, it’s really hard to manage as a third party. Especially a deal point like, “Make your service more user friendly.”

I would add, the other piece is building value in the eyes of customers. If a customer has to go to HBO Max’s application every day, they learn to value the content on that experience. In someone else’s streaming service that just doesn’t happen. It devalues the HBO brand overall.

- Pricing – I haven’t negotiated these type of deals in a few years, but if terms are roughly similar to then, which I believe they are, there is a big monetary difference between a channels revenue split–which is a monthly recurring payment–and a device “bounty” where the device owner gets a one-time payment for signing up new customers. The latter is an enticement to have the device owner market your platform; the former is a deal tax primarily. But they work out to dramatically different financial outcomes for a streamer. A 30% fee in perpetuity can be awfully expensive.

But that’s not all the revenue Amazon wants…

- Advertising – This issue came up with Disney+’s negotiations as Amazon wants a cut of advertising revenue from the apps on its platform. On the one hand, this is bonkers as Amazon will have very little to do with creating value from those ads. On the other hand, in the old MVPD world, cable channels shared advertising time with MVPD operators. (That’s how local ads made it on old school cable networks.) Given that AT&T has dreams to launch an ad-supported version of HBO Max, this is likely a huge sticking point.

- Content – Andrew Rosen thinks a big hold up is that Amazon wants Warner Media content for IMDb TV’s FAST service. I’m not sure AT&T would ever consent to this, but not long after Disney+’s deal was closed the same group licensed Disney-owned shows to IMDb TV. Consider the market power that when AT&T is trying to negotiate for a device deal for its streamer, Amazon is essentially demanding that some of the content for that service wind up on a competing streamer. Such is Amazon’s market power, that a deal term could be forcing a studio to sell it content. (As I wrote on Twitter, the echoes to Standard Oil are remarkable.)

- Data – AT&T also wants the customer data. If you don’t control the user experience, you don’t control the data either. They basically go hand in hand. For as much as I love data–look, it was the first theme of this website–I do think “data” has been a bit overhyped in the business sphere. Data is an asset, but it isn’t actually cash. It is something that can generate more cash, but only if you use it properly. Still since it goes hand-in-hand with user experience, they’re tied together.

The Major Streamers Don’t Allow Bundling

That’s really the issue for AT&T. Netflix, Hulu/Disney+ and now HBO Max see themselves as bigger than just content in someone else’s streaming application. Heck, even Prime Video content isn’t available in Apple Channels!

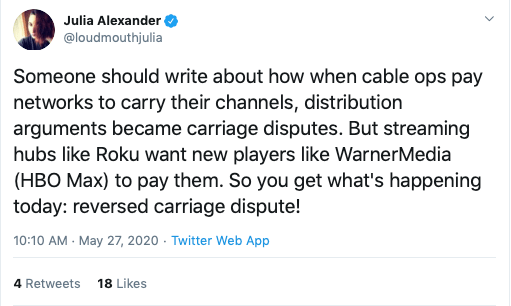

And when you think about it, the ask by Amazon is kind of crazy. It’s not just asking to sell rights to HBO’s content, it’s asking for that content to essentially be bundled with the rest of its content. Which seems a lot more like a retransmission issue than simply allowing an application on your operating system. The best tweet which summarized this for me came from The Verge’s Julia Alexander:

Exactly. Thus, the whole debate is fairly simple: AT&T considers itself a major player. And won’t allow itself to be bundled.

Who is right?

First off, no one is right or wrong. The worst thing in the world is to pretend like negotiations between two businesses are about fairness or justice. Or that the needs/wants of customers matter. (If you want the needs of customers taken into account, government regulation is your only hope. And entertainment should be heavily regulated!)

Still, who is more right in holding to their position in this negotiation? AT&T.

When in doubt, ask who is creating value. AT&T has decades of valuable content, is spending billions making more and will have to spend hundreds of millions more to market that content. In other words, they’re doing all the work to launch a streamer. Amazon is a gatekeeper asking for a fee/toll/rent to allow it’s application on its platform.

Not to mention AT&T bears most of the risk, unlike Amazon. To maximize that investment, they need to distribute and own that customer relationship. So they’re right to hold, and it will be fascinating to see who blinks first.

Other Contenders for Most Important Story

A few other stories filtered in over the last week that competed for the top spot. A few were generally interesting, but just couldn’t compete with the HBO Max drama.

DAZN Shops Itself

A report from the Financial Times says that sports streamer DAZN is looking to raise money, which could mean anything from selling itself to finding a strategic partner to simply selling equity. Of all the newly launched streamers, DAZN has the toughest road to travel. Sports rights are extremely expensive, meaning they cost almost as much as the value they bring in. As much as I’d like an “indie” sports streamer to survive, DAZN needs cash to compete with the tech giants of the world.

Quibi Programming Strategy Reset

Less than two months in and Quibi is already revamping its programming line up. The plan is to focus more on what is working, which is apparently content that appeals to older, female viewers

Is this too aggressive of a pivot? Maybe. This is the perennial problem with data driving content decisions. Quibi is looking at what is working on their platform, and using that to make future content decisions.

But does that make sense? If your two best shows happened to appeal to that demographic, then it will make it look like that’s your best customer demographic. If you use that data to make more decisions, then you’ll no doubt appeal more and more to older, female viewers.

Do you see how this is a self-reinforcing algorithm? And how that can limit your potential audience.

Want to see how this applies to Netflix? Well, they too made originals, but they also put originals on the top of their home screen. This drove usage, because anything on the top screen gets clicks. But then Netflix made more originals using that data, in a self-reinforcing loop. Hence, why some of Netflix’s content feels so similar or appealing to the same demographics.

Disney World and Universal Studios Plan Summer Openings

July 15th is the planned date for Disney World to reopen at half capacity with tons of restrictions. Universal presented plans as well. This is both expected and seemingly on track for the next stage. My tentative prediction is that as thinks open up, folks will return to old habits and behaviors quicker than currently anticipated. If testing continues to ramp up, we could find this surprisingly normal looking.

Peacock Originals Slate on July 15th

When NBC released their plans for Peacock, my initial reaction was Peacock wants to be the most broadcast network of the streamers. This review of Peacock on Bloomberg essentially describes that as the mission statement. And this made me happy because, in full disclosure, I think broadly popular content has mostly been missing from the streaming wold.

As Peacock prepares its first set of originals for July 15th launch, are we getting a broadly appealing set of shows, or are we getting another rebound of peak-TV/prestige content? Looking at the list of shows–a Brave New World remake, a David Schwimmer comedy and an international thriller–I’m worried it’s more of the latter. However, they do have Psych 2 special. So we’ll see.

Data of the Week – Nielsen Top 100 Broadcast TV Shows

Twice a year, Michael Schneider uses Nielsen data to look at the top shows and then networks for the previous TV season or year. Here’s the 2019 season edition, which feels so bizarre in today’s coronavirus times. I’m mainly looking at it for the next set of shows to come to streaming channels. Look for 9-1-1 to one day get a pay day on streaming.

Entertainment Strategy Guy Update – Apple Content Moves

Apple Snags the New Scorsese Film from Paramount…

This could have been my story of the week, but for HBO Max launching. Dollar wise, it’s relatively small. Just $200 million or so among friends.

But not with Netflix? What went wrong!!!

Likely the price tag and performance of The Irishman scared off Netflix. As I wrote in multiple outlets last December, Netflix doesn’t have the monetization methods to get a return on $300 million budget films. (That’s what I expect Netflix ended up paying for The Irishman.) Toss in all the controversy about theaters, maybe some DiCaprio nervousness about back end, and I think Apple TV+ with Paramount theatrical was the logical choice.

Is this good for Apple TV+? Sure. It will get a ton of new subscribers to check them out. Without a library, though, how long will they stay? Speaking of…

…and Fraggle Rock from Henson Company

Bloomberg reported last week that Apple was looking at licensing library content. Well, their first “big” purchase is Fraggle Rock’s library to complement an upcoming reboot. Then there was controversy in the entertainment journalism press about whether Apple had changed strategies or not. (Which would directly contradict my column from last week.) Apple PR went to multiple outlets to leak that “No, no, nothing has changed.”

My guess is both scenarios are true. If Apple can’t find a library to buy, they’ll say their strategy hasn’t changed. If they do? Then they’ll happily announce it.

Meanwhile, is Fraggle Rock a game changer? I doubt it. Kids need lots of content to go through. Almost more so than adults. Frankly, Apple TV+ doesn’t have it.