Disney is a marketer’s marketer. With the biggest brands in entertainment, they can serve up an investor day—an investor day that is for Wall Street investors!—that gets regular folks to turn in and trends on Twitter. Yet, for all the buzz, the basic story was that Disney is releasing Disney content on the Disney branded streamer. We’ll get to that, but another story could have bigger implications for entertainment.

(Sign up for my newsletter to get all my writings and my favorite entertainment business picks from the last 2 weeks or so.)

Most Important Story of the Week – The Antitrust Case Against Facebook

A few months back, following Epic’s Games epic lawsuit against Apple, I stated that I planned to follow “antitrust” news fairly closely. Because antitrust could be the new “deregulation”:

I’ve been scanning the landscape more over the last couple of months to look at the future. And the “blue ocean” space in the entertainment strategy landscape for me isn’t technology–again, the futurists have it covered–but how regulation could change business models. And this is a hypothesis I’m monitoring:

Could antitrust enforcement could become the new deregulation?

Deregulation was arguably the biggest driver of disruption in the 1970s and 1980s. Deregulating industries across the globe from airlines to energy to telecommunications repeatedly enabled smart firms to seize new advantages. That airlines example above is a perfect example; Southwest likely doesn’t become Southwest without deregulation.

Generally, everything has been deregulated. So what comes next? My guess is a reversal of antitrust.

Since then, the signs that antitrust is on the agenda have only picked up steam. Consider:

– The House Antitrust Subcommittee released the “Cicilline Report” which laid out how the four big tech firms have used their market power to hinder competition.

– The Department of Justice filed a lawsuit against Google for specific antitrust violations. State Attorneys General are expected to follow suit.

– Joe Biden was elected as the next President of the United States. While there is some bipartisan support of renewed antitrust legislation (see Google’s antitrust suit, filed by a Republican), Democrats are still clearly more supportive than Republicans on antitrust.

– This week, 48 states and the Federal Trade Commission filed an antitrust lawsuit against Facebook. (Also a bipartisan move.)

In August, I laid out a few waypoints that I would watch to see if increased antitrust enforcement was likely coming. We hit the big one (Biden’s election), the next biggest (Congress increasing pressure) and now antitrust is headed to the courts (Specific lawsuits against Google and Facebook). As the future becomes slightly clearer, then, it’s worth expanding the potential for what comes next, especially for entertainment and media.

Predictions

What happens next?

To start, more antitrust lawsuits for the rest of big tech feels inevitable. Amazon seems particularly easy given that they have leveraged their market power in retail for years to enter new industries or stifle competition. The complaints from smaller vendors are legion. (The diapers.com affair from the start of the decade is particularly egregious.) Apple is more beloved than Amazon, but the Fortnite fiasco basically illustrated in stark terms Apple’s market power, and brought up a host of smaller competitors crushed under their power. Both Amazon and Apple, though, are more popular than Google and Facebook, which have both been embroiled in partisan bickering.

After that? The states/FTC/DoJ will either win or lose their lawsuits. That proposition is dicey because these suits are decided by individual judges, many of whom were appointed by Republican presidents with The Federalist society backing “Borkians” who tend to downplay antitrust concerns. Or in some cases just don’t believe antitrust is worthy of government attention.

If the states lose their lawsuit, then it would require Congress to change the laws around antitrust. That’s a much tougher challenge in today’s political landscape. But not impossible. (The Georgia run-offs will say a lot on whether this is possible.) Assuming that the Big Tech companies lose their fight, then come the potential remedies, which adds another layer of complexity to predicting what happens next.

Potential Outcomes

Let’s be honest and let the air out of the balloon right off the bat: The most likely outcome is that Big Tech is mostly left in place. Think Microsoft in the 1990s. In the worst case, the companies agree to some measures to control their behavior, but immediately go back to not following them and paying minuscule fines.

This is, essentially, what has happened with most merger consent decrees this decade. Facebook said it wouldn’t integrate What’s App’s data, then did it anyways. AT&T said prices wouldn’t go up after mergers, then raised prices. The companies pay the fines and keep consolidating. Disney said it would keep producing Fox movies, but now may release fewer films in theaters post merger than they did before.

The best case would be consent decrees that are enforced. Like the Paramount Consent Decrees of the 1950s. This helped movie studios and theaters thrive. Or AT&T’s forced divestment of patents in the 1950s. This spurred innovation across the U.S. landscape, which really did help competition. (It does say something that success examples of this happened 70 years ago…)

The bigger, and more fun to imagine, scenario is breaking up big tech. (And while I try to avoid my own policy recommendations, this is the outcome that I believe would benefit America the most.) These breakups could be either horizontal (the same industry) or vertical (different business units in the same company in related fields).

Vertical is actually easier in most cases since the different companies don’t need each other to survive. So for Amazon, spinning off AWS, for example, would hardly impact Amazon’s retail business. (Though it would deprive Amazon of a valuable profit stream.) Google has multiple business units that could easily survive on their own. I’d add that splitting up Instagram and What’s App from Facebook are horizontal break ups, but relatively easy to contemplate since customers wouldn’t notice a change. (I’d make the same case for Amazon breaking up their marketplace from their other retail enterprises.)

While vertical break ups in many cases don’t address market power, they are still very helpful for competition, since it means the firms left in a given industry can compete more evenly. (And most vertical integration tends to be followed by price gouging, product tying or other anti-competitive behavior.)

The key question for entertainment is whether each of the big tech titan’s entertainment enterprises get divested individually or remain as part of the bigger conglomerate. I could argue that Google should easily divest Youtube. Youtube can clearly survive on its own, but this would also give a powerful new internet advertising option to marketers. Apple could divest its media fairly easily (they are all just apps running on their operating system). Amazon has a better case for Prime Video staying in Prime, but even that isn’t ironclad. (Ask yourself: couldn’t Amazon pay the new Prime Video to stay in their Prime bundle? Yes, obviously. So why wouldn’t they? Because the value isn’t actually in the current video/data, it’s the market penetration to gain dominance overall.)

This is an unlikely scenario I’ve laid out. The plaintiffs have to win their lawsuits and then the remedy has to be the most extreme of remedies (break up). But imagine we do get here. Who are the winners and losers of this world? Imagine that Prime Video becomes its own company (with Twitch, Amazon Music, Audible and maybe a few other assets). Apple One becomes its own company (Apple Music, iTunes, TV+, Arcade and so on). And Google spins off Youtube.

Who wins or loses in this scenario?

Winner: Netflix

Say what you will about being bearish on Netflix’s business model, they aren’t a monopoly. Some investors want them to become one (building a “moat”), but a company with only 8% of all viewing in the United States is hardly a monopoly. Indeed, the biggest threat to Netflix, in my mind, is the unlimited cash reserves of Apple and Amazon. If forced to compete on an even playing field, this would benefit Netflix. (With the caveat that multiple new streaming companies on the NASDAQ may impact all share prices simultaneously, for good or ill.)

Winners: Traditional Streamers

Cord cutting is the biggest pain point for traditional media. But the biggest challenge, more than anything, is competing against competitors who don’t have to make money. If Big Tech had to compete on a level playing field–read not deficit financed–traditional media has a much better chance to survive in a streaming world.

Further, there is a big difference between radical disruption (where revenue drops by double digits year over year), and slow evolution (where profit margins slowly decline). Both get to the same place (which is the likely outcome from streaming), but one has a lot less pain for the incumbents and their suppliers.

Losers: Prime Video and Apple

These seem like the two biggest losers in all this because most folks acknowledge that their streaming business models just aren’t based on actually delivering a valuable product. Phrased differently, no VC firm would invest in Apple TV+ if it weren’t owned by Apple; there is no business plan there. Spun off from their parents, these new media companies would be valuable, but much less invincible.

Losers: AT&T and Comcast

After Big Tech, if Congress wanted to find the industries that are heavily consolidated and hated by customers, cellular and cable are next on their wishlist. (Then health care.) Breaking up Big Cable would probably be the most popular move of the Biden administration.

Winners: Roku and Sonos

If devices are sold at cost, the independent device makers have a chance to succeed and thrive.

Winners: Talent…probably.

In a lot of ways, the boom of streaming and peak TV is the best of times and the worst of times for talent. More shows and films are being made than ever before, but back end cuts are smaller than ever before. Meanwhile, junior writers work for some of the worst pay in the last few decades. Arguably, with many more streamers who are less powerful, the guilds could negotiate better rates, especially down the line.

However, this may be offset by the end of the so-called “Drunken Sailor Era” (™ Richard Rushfield) as firms have to start making actual money. So they could cut back on content spend. That means less potential jobs overall.

TBD: Customers

Like talent, this could go either way. On the one hand, it has been great for customers to have multiple firms willing to subsidize cord cutting. The problem is those subsidies are harmful long term and entrenched market power is awful too. So prices could go up, but they’d reflect economic reality. Meanwhile, customer choice would come either way.

The Caveat: All of this is Unlikely

Does a huge break up of Big Tech, including spinning of media firms actually happen? Probably not. But without throwing out random probabilities, it’s probably twice as likely as it was even in August. (So yes, this is like a streamer saying a show grew 50% year over year. 50% of what?)

Yet, Biden was elected President, and that’s huge. Combined with renewed emphasis by the Democratic coalition, and I think corporate consolidation is on the table for change. He’ll likely appoint attorneys general, federal judges and administrators who could put a renewed emphasis on antitrust. That will impact entertainment eventually.

Other Contenders for Most Important Story

Disney Investor Day

Few analysts are (and have been) as bullish on Disney’s streaming future as I have been. I write that to put in context what I’ll write next: I don’t think this Disney Investor’s Day deserves the hype it has been given.

Take a few of the headlines touting “10 New Star Wars and Marvel” series coming to Disney+. That sounds huge. But given that this will take place over the next few years, is it? In context? Take this analysis by Emily Horgan:

On Marvel, I don't think so. Looking at 2016 – 2019 they had 11 movies, 11 active Live Action shows across ABC and Netflix and 7 active animated series.

— Emily Horgan (@emohorgan) December 11, 2020

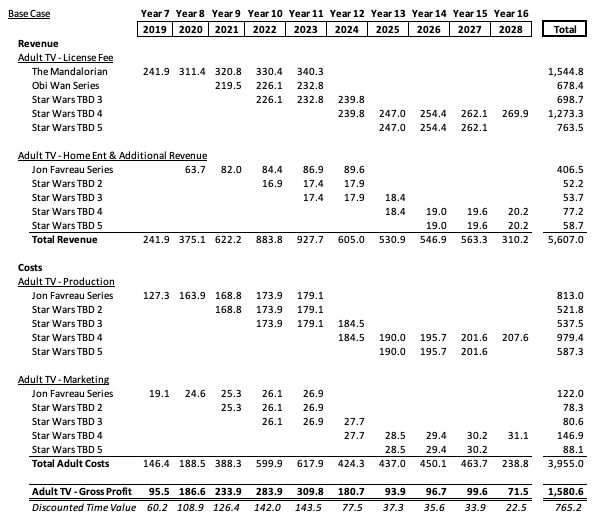

Or take my timeline I’ve been using to model Lucasfilm’s financials:

And for kids…

In other words, Disney confirmed what I’ve been modeling for a while now. This Star Wars volume is a pinch higher, but considering the volume of one-offs, not that much more than I modeled. But most of Wall Street/the trades seem surprised by it. I’d add there are a few more caveats for why the total volume of content may not match the reality:

– Shows will likely get cancelled. Like Ghost Rider, Benioff and Weiss’ Star Wars Trilogy, Howard the Duck, Rion Johnson’s Star Wars Trilogy, more Han Solo films, and countless other projects over the years.

– A lot of this content is animated and for kids. Which is crucial to Disney’s future, but likely replaces exactly what they were making for Disney Channel, Disney XD and Disney Junior. Which we weren’t getting super excited for before streaming times.

– Some of the announcements really are for a long way off (like a Rogue Squadron film in 2023). Most announcements didn’t have dates.

In total, then, I don’t think this is really much more content than Disney was planning on making last year or the year before. Some of it may have shifted from film (previous pitches for movies may have turned into TV series, like potentially Obi-Wan), but it’s probably similar. At the end of the day, it looks like from 2021-2023 we can bank on a Disney live-action adult series every 2 months or so on the platform for Marvel and Star Wars.

January-WandaVision

March-Falcon/Winter Soldier

May-Loki

Summer-Marvel What If?

Fall-Ms. Marvel

Fall-Hawkeye

Christmas-Mandalorian S3That's what I gathered for 2021, which means there would be consistent flow of tentpole content for the year with even more in 2022.

— The Streaming Wars (@StreamingWar) December 11, 2020

That feels about perfect. If they can keep up the quality, that’s a big slate that will keep folks subscribed. It’s also the “if” that defines all success in entertainment.

(Though Disney+ still has a big hole for adult TV outside of Marvel and Star Wars. That’s a tough hole to fill.)

As for business strategy, the biggest news is no news. Hulu stays where it is. Star is officially becoming Disney’s adult brand globally. ESPN+ will continue expanding, and be available within Hulu. And lastly only one film is “breaking” the theatrical window, with Raya going to Premiere Access (like Mulan’s $30 release) simultaneous with theaters. (I have a feeling it will do much smaller business than Mulan on PA.)

An NFL Update: Ratings are Down, but Good for Broadcast

Is the state of the NFL viewership good or bad? Maybe both. Americans consume NFL football more than any other sport–arguably more than any other type of content period–yet the ratings aren’t as high as past years (down about 8%) because linear TV viewing just isn’t as high as it was (down about 30%). This of course begs the question for what happens next. I can’t see a world where broadcast TV doesn’t nab a few more years of NFL rights, even non-exclusively, but the key question is, “At what price?” Likely they will be high.

Disney+/HBO Max and Comcast Integration

Disney+ and HBO Max will soon be available on Comcast’s Flex operating system. This is a smart next step for both Disney+ and HBO Max. (If anything it should have come sooner.) For all the talk of cord cutting–and there is a lot!–one of the surprising survivors is the cable box. This makes it much easier to reach another big group of customers that Netflix and Prime Video are already reaching.

Data of the Week – The Hallmark Channel Is Still Winning Christmas

Josef Adalian has the details in a recent newsletter, but 3.4 million folks tuned in on one Sunday for a Christmas movie. Linear TV is dead, but it won’t lie down.

M&A Updates

Just because antitrust is back on the agenda doesn’t mean that mergers won’t continue fast and furious. The two latest biggies both have tangential relations to entertainment. Slack is the de facto messaging service of lots of Hollywood, and it was just purchased by Salesforce. Meanwhile, S&P and IHS are merging for a huge price tag because they are both financial data firms. S&P fascinates me because they had earlier purchased SNL Kagan, and Kagan was a tremendous source for entertainment data back in the day.