We’ve ended the “Asterisk Extraordinaire Earnings Season”. Giant tech companies did well; lots of other folks did poorly; what happens in the future is up in the air.

One company that did particularly poorly was The Walt Disney Company, which wasn’t much of a surprise, given that all their theme parks were closed, so were the theaters they use to release their big budget films and their flagship channel ESPN didn’t have live sports. No company was more exposed to “quarantine of everything” than Disney. Well, maybe Live Nation. (Of course, since Disney beat their “expectations” their stock price went up.)

The story that caught my eye–and many folks on Twitter as well–was the news about Disney’s plans for Hotstar. Which is unique enough to be my…

Most Important Story of the Week – Star (nee Hotstar), Hulu and the Perils/Promises of International Growth

The news is Disney plans to turn Hotstar into a global streaming service.

For those who don’t know, Hotstar is an Indian SVOD company that was part of 21st Century Fox and the Murdoch empire. It is owned by Star in India, which is a wholly-owned subsidiary of Disney. Lots of insiders noted at the time that while Fox had a lot of buzzy assets (Simpsons, X-Men films, FX), Hotstar could have been the secret, undervalued asset since it’s the biggest streamer in India, despite fierce foreign competition.

Indeed, when Disney launched Disney+ in India, they used Hotstar to give it a boost. To simplify, Hotstar is to India what Hulu is to America: a broad general entertainment service. India, then, is another example of Disney using multiple streaming services to provide a general entertainment bundle. (Star also has lots of sports rights.)

The news this week is that Disney plans to use Hotstar–referring to it as “Star” in their earnings report, presumably the new global name–as its new global, general entertainment brand. Many assumed that Hulu would have this role, partly because even Disney said Hulu would eventually roll out internationally, sometime in the 2021 calendar year. And when they clarify “calendar year” that means Q4, since their financial year starts in the fourth quarter of the calendar year. (I had thoughts for how they should optimize their next round of streaming launches here.)

This news is a bit surprising. With the onset of Covid-19, Disney said they were delaying Hulu’s international rollout. Presumably that meant all global streaming ambitions.

Apparently not!

In other words, Hulu is out and Star is in. It wasn’t about saving money, it was about changing strategies.

Star has some advantages over Hulu. First, Hulu is still partially owned by Comcast for a few more years, and that means they have some input into how it operates/makes/loses money. Second, Hulu doesn’t have an international footprint, so it doesn’t have any advantage over Star in branding. Third, since Hulu isn’t global, it doesn’t have international rights for most of its content, which means again it has no advantage in launching globally.

Whether it’s Star or Hulu, clearly Disney wants to be not just a US or Indian only streamer, but a global streamer like Netflix or Prime Video. And the reason is to take advantage of what Netflix (and its boosters) call “global scale”. The idea that if you make content and sell it globally, you can amortize it over a broader swath of customers, hence increasing return on investment. For this strategy to work, it means content in one area has to travel well globally.

The complication is that not all content travels well. In fact, I’d estimate 90-99% of content does NOT travel well. Yes, this clashes with the rhetoric coming from Netflix and Netflix analysts that tout the streamer’s global scale. This frankly just isn’t supported by the economics or the data. (Do I have a half-written article on this that I haven’t published yet? Yes, I’ve been working on it for two years.)

The content that does tend to do well globally is relatively narrow, with some outside exception:

– Big feature film blockbusters produced in Hollywood

– Animation (Because the voices can be easily dubbed.)

– Some procedurals produced globally (Think police dramas.)

– Some soap operas produced globally. (Think telenovelas or K-Dramas.)

– Some broad comedies (The key is not niche or culturally specific humor.)

This is my big worry for Disney’s global plans. Both for Hulu when it got delayed and now for Star. Essentially, they’re building a global service off primarily American originals and American productions. Don’t take my word for it, here’s Bob Chapek:

The worry is that FX prestige dramas don’t play in Indonesia. Same for Searchlight indie darlings. And the same for broad-based comedies produced by Disney-ABC Television. As an American, I’m in for these types of shows. But I understand, and have seen, that different cultures want content produced by that culture.

Does Disney have broad, tentpoles for a service like this? Yep. If you want global content, nothing better than this:

And toss in the wildly popular globally Simpsons. But that content is already on Disney+. So what does Star offer to customers if Disney+ is really the globally appealing service? Sure, it can bundle Disney+, but then why would customers who aren’t in India want/need Star?

My Recommendation: Take The Middle Ground: A “Regional” Streamer

If I were advising Disney, I would ignore the not-actually-working-in-practice theory of “global scale.” It’s a mirage. Instead, I’d focus on content that travels “regionally”. My suspicion is Disney knows this and that’s what Star’s actual mission is.

See, between content that doesn’t travel at all and content that is globally popular is a third type of content: “regional” content. This content travels within certain language groups or cultural areas.

For example, Bollywood dramas play well globally. They just don’t travel to markets like America or Europe. But they perform across South Asia, the Middle East and larger Asia. If this type of content was paired with TV content from America that does travel well, you could begin to see a service that targets those regions fairly well. Then you could top it off with Fox/Disney blockbusters that don’t fit on Disney+.

Of course, then Disney would need European-focused content for Star in Europe and Spanish content for S Star in Latin-American focused service and so on. In other words, no global scale.

Long term, this strategy would get about as many subscribers as Netflix has globally, but would be more sustainable from a cost perspective. (While having less upside from the perceived advantages of global scale” for the stock price..) Instead of repeatedly overpaying (sometimes by 100%) for global rights, Disney could slightly overpay for regional rights, focusing on the territories most likely to actually watch a given show. (Again, I’ll prove this argument in a future article.)

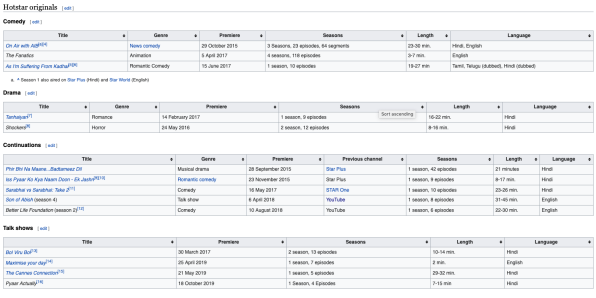

Let’s bring this back to Hotstar/Star. I’m by no means an expert on their content, but from what I can tell, they don’t have a lot of original programming to act as the driver of even regional content growth. Here’s from the Wikipedia page.

On the flip side, its parent company Star does have original production studios. Presumably with some content they can leverage globally. Again, I’m not an expert in Indian TV production, but Chapek mention it in their plans.

Final call? For the big news of the week, if the question is “good strategy or bad strategy?” for the moment I have to say, “It depends.” Disney is clearly launching something globally and Star seems to be an easier brand to do that with than Hulu. But it’s far from a sure bet.

Data of the Week – Peacock has 10 Million US Sign-Ups; Disney+ Has 60 Million Global Subscribers

Peacock’s 10 Million “Sign-Ups”

Is this a good number? Like last week, I don’t know. More than any other streamer, Peacock is a work in progress. It’s biggest tent pole–the Olympics–was delayed a year. Hopefully Comcast will keep releasing these sign-up numbers every quarter.

Likely NBC-Universal saw a big jump in sign-ups at both launch (Comcast/Cox in April, national in July) based on the advertising campaigns. My guess is new sign-ups will slow until the Olympics and look like a shape I’m calling “the substack curve”. The question is when they can get their next big leap in subscribers. Unfortunately, that’s probably not until next year, at the earliest.

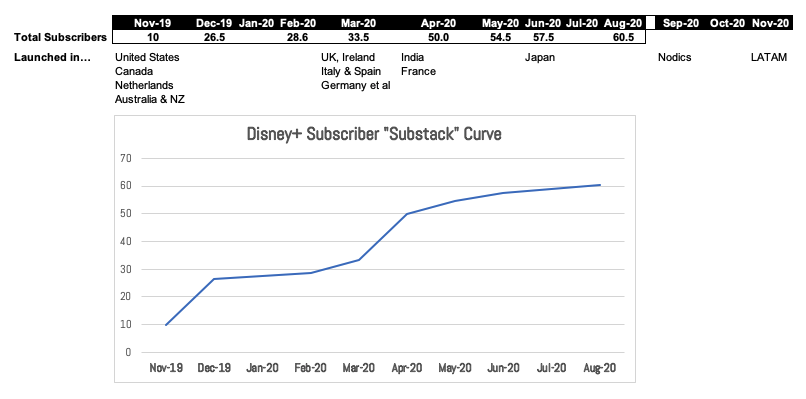

Disney+ Subscribers: Did Hamilton Help?

Disney announced a Covid-19-driven boost in subscribers. Here’s how Disney’s subscribers have grown over time:

Thankfully Disney wants to keep winning headlines, so after each earnings report they provide updated Disney subscriber numbers. This enables us to see a nearly monthly growth in subscribers for the streamer.

Someone pointed out that for all the buzz of Hamilton–here’s one analysis saying more folks have streamed it than seen it in person–it didn’t actually move the needle in subscribers. (For instance, I said it “won” July over at Decider based on this assumption.) From June 27th–when the earnings report came out–to Tuesday’s earnings call, Disney “only” added 3 million subscribers. Some points on this interesting theory:

– My guess is 3 million is still quite a lot to add in one month. As their subscriber chart shows, the only other time they’ve beat this number of additional subscribers is when they launch in new territories.

– As Hamilton was one of only a handful of shows to launch in July, it’s a lot easier to triangulate how many new subscribers it acquired than it is for any given Netflix show. (We also don’t have official monthly subscriber numbers for Netflix.)

– Some of the subscribers likely did “churn in and churn out” of Disney+. Meaning they signed up for a month, watched all they wanted and cancelled. That’s the new reality for streamers, and I include Netflix in that.

– We don’t know the “null hypothesis” meaning we don’t know how many subscribers Disney+ would have had if they didn’t move Hamilton. Essentially, this isn’t an “experiment” because the control group can’t exist. If Disney hadn’t released Hamilton, maybe Disney+ would still have ended up with 60.5 million subscribers or maybe they’d have stayed at 57.5 or somewhere in between. We don’t know.

– The blockbuster strategy is still the key for Disney. Those blockbusters need to be successful TV series based on their IP. I’m looking at you Falcon and Winter Soldier.

Other Contenders for Most Important Story

AMC Networks Announces Earnings

The headline is that ad sales are down, which isn’t surprising. The sub-headline is that due to Covid-19–asterisk extraordinaire–AMC is ahead of its goals for its multiple niche streaming services.

For a good take on the state of AMC, I recommend this recent episode of TV Top Five about the departure of Sarah Barnett.

CBS All-Access Expansion is Coming! And globally.

News continues to slowly leak out about SuperCBS’s plans to revamp CBS All-Access into a broader, Viacom-centric service. Notably, lots of episodes of Viacom programming are now available in CBS All-Access, though in many cases not current seasons due to ongoing licensing output deals. (Read the details in this long interview by Scott Porch at Decider.) Meanwhile, it’s collection of various niche streaming services does not seem to be going anywhere either.

Then late yesterday, CBS announced its new plans for a yet to be branded Viacom-CBS global service. It’s a combination of Showtime, CBS and Viacom content, sort of like what you’d expect CBS All-Access to become.

Overall, the Super CBS strategy continues to not be well-defined, to not focused vision and to not build a competitive advantage. (That’s bad.)

Pluto TV and Verizon Deal to Offer PlutoTV

According to Deadline, the partners in this deal consider it ‘game changing”. And I can see their point: Pluto TV will be preinstalled on plenty of new phones and TV devices. (Notably not Apple devices.) That said, Pluto TV is and has always been “free”–it’s the F in FAST–so it’s not like as much money is changing hands as the Disney+/Verizon deal.

Lots of News with No News – Tik Tok Sale & Instagram Reels

My favorite hobby is pointing out that America’s tech giants are fairly poor at innovation. Indeed, most of the news businesses launched by Google, Facebook, Microsoft, Apple and Amazon are shockingly similar to smaller companies’ business models. The latest is Facebook taking aim at Tik Tok by launching “Instagram Reels” a thinly veiled video copy of Tik Tok.

Meanwhile, Microsoft is negotiating to buy Tik Tok for somewhere between $30 billion to a trillion dollars. (Last number is fictional.) Judging by my newsletter feed, some folks consider this clearly the biggest business story in America. I’m not there yet, but will monitor if a sale happens.