This week my head has been deep in the data of the streaming wars for my latest article for Decider. I reviewed multiple different data sources to sort through the content of the last two months. Go read that article if you haven’t yet to know who won September!

Overall, the political news of the week overshadowed major entertainment stories. But one story has intriguing long term implications.

(As always, make sure you subscribe to my newsletter, which goes out every two weeks. It’s the best way to make sure you don’t miss my writing.)

Most Important Story of the Week – Google’s New Chromecast (and Netflix Offer)

Google’s first Chromecast is probably underrated for its role in the streaming TV revolution. Instead of needing a fancy new box or “smart” TV, you could plug in a small device into the back of your television and stream Netflix to your living room TV. Even if a majority of cordcutters opted for a better solution long term (usually a Roku), I think Chromecast was the hook folks used to sample streaming on TV. (It was also cheap.)

It’s been rumored that Google was working on a next generation Chromecast or TV device/operating system, and this week we got the announcement. Here are the key details, with the caveat that I haven’t actually used the new device, and am going off reporting on the announcement:

– Google TV is the interface built into the new Chromecast.

– At launch, HBO Max, Disney+, Netflix and Youtube TV are available, with Peacock coming soon.

– The ability to search for content is the pitched differentiator of this service.

– They are bundling the service with a Netflix subscription for one year.

– You will still need to watch content in the streaming applications themselves, like with Apple or Amazon. But the new Google TV app puts all the content in one place.

So what do we make of this? A few things. Here are my hot takes and some others.

Devices Are Key…

Thanks, Captain Obvious.

In TV, someone is always going to be the rent seeker, placing themselves between customers and content. Previously, it was cable providers. But now Roku, Google, Amazon and Apple are playing that role. Hence why Peacock and HBO Max are still fighting to get on Amazon at terms they can agree to.

To truly grab the attractive profits, these device makers are desperately trying to control the user experience. They’ve all started with similar/identical abilities to search for content and have it all aggregated on the home page. While they tout it as revolutionary–Google pitching search–it’s still mostly the ability to search content from a variety of channels/apps in one place.

..but the True “Aggregeddon Scenario” Hasn’t Happened Yet

That’s the scenario where you watch The Mandalorian in Google TV and then Stranger Things autoplays right after without the user needing to leave Google TV. Why is this such a hurdle? Because it is the whole value proposition. And the streamers know it.

If Disney+’s content is branded with everything else in streaming, then given shows no longer build Disney’s crucial brand equity. If Netflix can’t have its algorithm sell on you another show, then it loses all the value of its honed algorithm. If Peacock can’t offer you their linear channels while you’re watching Parks and Recreation, then their value proposition takes a hit.

The big tech giants know this, and want to take all that value for themselves. The golden goose is to be the sole provider, which makes all the content providers simply commodity brokers. So far, Netflix, Disney, HBO and others have held off on this, and it will be curious to see how long it lasts.

Will Folks Criticize Netflix for Getting Cheap Subscribers?

They won’t. Though the narrative would be more accurate if they did.

Netflix has been as aggressive as Prime Video, Disney and HBO Max in courting subscribers with free subscriptions bundled into other services. (Notably T-Mobile for years, a subscription many customers didn’t know they had.) This is a bad thing for Netflix; without knowing the deal terms, my gut is Google is paying nearly full-freight on this deal because they have money to lose and market share to gain. If this helps keep Netflix subscribers stable through 2021, it’s a good idea for the streamer of record.

From Parqor: This is the Search Engine Interface

I like this take, because no one uses Google search data more than me. And while it isn’t perfect, it is a great signal for “interest” in a given topic. Moreover, Google’s extremely big advantage in search–over say an Apple or Amazon–they really could make a smarter search at driving to shows folks want to watch. As such, I’d give them a leg up over Apple in the smart TV race. (Though behind Amazon and Roku, who have been doing better for longer.)

Entertainment Strategy Guy Update/Data of the Week – Mulan’s Data Update from Nielsen

The other contender for most important story of the week was Nielsen’s SVOD Top Ten list this week. (Did I write it up? Yes. Will it be an article on Tuesday next week? Yes too.)

Because one detail in particular shocked me:

Mulan made the top ten list!

(As a note, Nielsen delays their SVOD rankings for four weeks while they calculate. And no, I’m not a Nielsen skeptic. Their data is very useful.)

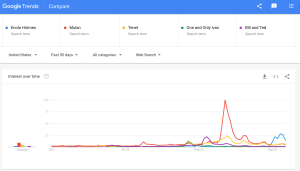

For a single movie to go up against shows with dozens of episodes really does show the demand of Mulan. On one hand, this matches the Google Trends data, which showed that Mulan was really popular. Look at this take from my recent Decider article, where Mulan is multiple times more popular than Enola Holmes, which is the current Netflix popularity champion:

Still, when I did some quick math (like LOTS of folks on Twitter), I got really worried. If 525 millions minutes were consumed of Mulan, divided by 120 minutes as the rough length of the film, then that means it was watched over 4.5 million times. If each household purchased it per viewing, that’s 4.5 million purchases, nearly 4 times what I calculated.

Yikes!

Calm down, calm down. See, like all things, we just need to get everything back to apples-to-apples. Nielsen is measuring minutes viewed, but we were estimating purchases. That’s essentially two different ends of the customer journey.

To think through it, it’s worth first considering the user behavior that influences how many folks actually watch a show. (Some of which I thought of, some of which users on Twitter pointed out.)

– First, customers have to buy it. That’s what we’re trying to estimate.

– Second, they have to watch it all the way through.

– Third, they can choose to rewatch it or not. If they loved it, they will.

– Fourth, they can share their account with others, who can also watch the film.

When I analyze data, I alway think back to the customer use case first and foremost. It helps ground the data thinking in the real world, as opposed to number cherry picking. In this case, all these factors could influence how much the 4.1 million viewers actually relate purchases.

The next step is understanding how Nielsen got to their number. They measure the average minute audience, the way they always have. Then they multiply that by the length of the film, and boom they get the total minutes viewed.

But there is one more key: Nielsen estimates how many folks are watching a given minute of television at home. So if two folks are watching, that counts twice. (2 people watching 1 minute is 2 minutes viewed and so on.) (I reached out to Nielsen and they confirmed this analysis on background for this article.)

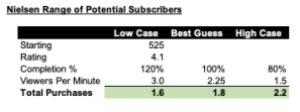

Combine these two and we have a way to estimate purchases. After we calculate the rating, we then estimate the completion percentage (which accounts for folks watching it multiple times or not finishing it) and then we estimate how many folks watched simultaneously. Here are my back of the envelope maths on it:

And thus we’ve taken Nielsen’s numbers and derived the potential purchases. For me, 3 people simultaneously viewing is high, but I could be talked into a higher completion percentage given password sharing. However, the high case feels unlikely, and I’d put it more like 2 million. 1.5 views per purchase feels fairly low as this was a family film. It also probably had a completion rate close to 100% than 80%.

With that, let’s compare this to our past estimates:

Where does that leave us? Well, on the high end of the estimates. Meaning that even under the most pessimistic circumstances for Disney (120% and 3 people per minute viewed) Disney would still sell 1.6 million units.

In all, this pulls my model upwards. If you’re taking a poll of polls, this says that Mulan had a better opening weekend than we initially suspect. So let’s assume Nielsen is the most accurate, and that means Mulan was purchased about 1.8 million times. That was my “high case” last time, which is more likely. Here’s a reminder of that:

Simply from a rhetorical standpoint, getting over the $50 million US opening weekend and $250 million lifetime revenue total would feel like a win for Disney. If this is the case, I’d expect they would tell us on investor day. Nielsen’s data makes this high case more likely, or somewhere closer to it.

As always, this is a story I’ll keep monitoring.

Other Contenders for Most Important Story

China’s Box Office Has Rebounded

Read all the details over at Forbes via (oft cited by me) Scott Mendelson. He pointed out that this partly dispels the myth that Hollywood relies on China for its grosses; arguably Hollywood needs China, America and the rest of the world to support its releases.

Disney is Laying Off Theme Park Employees

After calling for California theme parks to reopen last week, Disney announced layoffs this week for its theme parks in CA and Florida. Obviously, Florida layoffs don’t have to do with California being closed, but clearly Disney is hurting.

In the last week there has been a mini-surge in new layoffs across industries, with Disney joining others like airlines. Further, while the jobs report for September was another unemployment rate low since the pandemic started, there are serious questions about continuing that trend. Moreover, while the rate dropped, the number of new jobs was anemic. Mostly, folks stopped looking for work. That’s bad.

The Future of Smaller Films is Bright

If you’ve been following the film news, it’s been a dark few weeks. But smaller films (formerly independent) may have a surprisingly bright future. At least in the short term. After a few years lowering their spend at Sundance, Netflix went big at the Toronto International Film Festival:

![]()

Then you see this sub-headline about Paramount Network.

![]()

Of course, these films will be smaller in budget than big blockbusters. And that’s key: with limited windows, you have to have limited production budgets. Made for TV budgets. That’s something Netflix doesn’t do, but is slowly learning the lesson.

M&A Updates – Quibi is Up For Sale

Somehow last week I forgot to mention that everyone’s favorite streaming punching bag was up for sale. Welcome to the auction block Quibi! It’s unclear how much they are actually worth and how many assets they actually own, but you know a few firms, big and small, are kicking the tires.