Here’s why this week’s column is late. I started writing a Tweet thread, and then it went long. So I moved it to this column. Then that went so long, so I moved it to its own post. (Fingers crossed Wednesday.) So I’m starting from scratch midway through the weekend.

What was the formerly number one topic? Last week, when I wasn’t thinking about Disney, I was thinking about the debate over “niche” versus “broad” in the media ecosystem. So much so–and with news about layoffs, profitability and the general opinions on the future of media–I had anointed it this week’s “Most Important Story”. So what second place article climbed into the top spot?

Most important Story of the Week – Lionsgate (and hence Starz) moving on from Chris Albrecht

Consider this my “check in” with Lionsgate. I haven’t written much about this once high-flying studio–late 2000s Lionsgate was the mini-major king of the world–and Albrecht leaving after some internal turmoil gave me an excuse to check back in.

To overly summarize, they faced a common challenge of movie studios since the 1990s: replacing two great franchises, after milking them for what they could. In Lionsgate’s case, they haven’t found anything that approaches the highs of Twilight and Hunger Games. With some great ROI on the Saw franchise. (Warner Bros. had a similar challenge on an even greater scale with Lord of The Rings and Harry Potter.) Lionsgate has also tried to take advantage of the boom in “prestige TV” and “peak TV”. Though, to date, it seems like their main hit has been Orange is the New Black, with not a lot of other huge hits.

Their prospects in 2019 look better than 2018–where they only did about $388 in domestic box office–but they still don’t have a billion dollar franchise, with John Wick 3 as their best bet in 2019..

If your studio isn’t flying high, of course, your strategy can always be “M&A”–reminder M&A isn’t a strategy–and so Lionsgate acquired Starz in 2016. I liked this deal at the time. It gave Lionsgate a toehold into the streaming wars. Now, Chris Albrecht leaving isn’t the end of the world–very few executive team departures are, which someday I’ll write about–but it does show the challenges incorporating even a smallish entity into a larger one. We’ll see this with Disney and the impending 4,000 to 5,000 layoffs expected there. (More on that later.)

Speaking of M&A, I still expect that Lionsgate’s long play is–and has been–to let someone else buy them after getting a big enough return. They’ve been floated to be swallowed by Amazon more than anyone, though when it comes to M&A, I think guessing on eventual suitors is usually wrong more than right. Even if M&A may not be a strategy, it is still really hard to pull off.

If I had a pitch, instead of Amazon, I could see a fit with Comcast-NBCUniversal. Hear me out (and read my predictions of a super-consolidated future for more insight onto my thinking). First, Universal as a movie studio is facing the combined Fox-Disney behemoth, and this would give it another mini-major (with Dreamworks animation) with some franchises to try to leverage. But really Comcast does this deal to get Starz. NBC-Universal has a great cable portfolio it will use for its ad-supported streaming service. But it doesn’t have an HBO like Warner or Showtime like CBS. Starz would give them a “prestige” platform as the expensive add-on to the base model in their streaming service. (And more leverage in the digital retransmission wars to come.)

Would this happen? Again, with M&A it’s tough to say. Brian Roberts likes buying things, but for that reason Comcast has a lot of debt. Also, the government may grant mergers to Disney, because the current president likes Iger and Murdoch, but has already said it may relook at the Comcast merger, possibly because MSNBC/NBC News has reported bad news on the president.

ICYMI – My Articles from The Last Two Weeks

I spent the last week going all out to finish my series on Lucasfilm. My dramatic conclusion dropped and the answer is, Disney crushed it. Here’s the best table that summarizes what I found:

So take a read here (for building the final model), here (for my thoughts on the terminal value) and here (for my summary of the whole thing) including how much Disney would make without theme parks, Lucasfilm’s present value and the break even date. And spread the word to anyone who wants to know how to value an M&A deal beyond narratives and try to calculate the specific impact.

M&A Updates – Gimlet bought by Spotify for $230 million

This was the big headline of the week. (Getting StraTECHery coverage is my rule of thumb on this measurement.) It also pushed back slightly on the “media is dead” narrative, if you think media includes podcasts. (I’d say yes.) Spotify paid a huge price for Gimlet, but everyone seems to be pointing to the Anchor acquisition as the real win. This big deal comes on the heels of the announcement that Spotify is finally making both profit and positive cash flow, and the podcast acquisitions (with more to come) will deliver the next iteration of growth.

The challenges for me are twofold. (And yes, it is my job to be the one skeptic in entertainment business coverage of the tech companies. Read another positive take on Substack by Web here.)

First, it is a possible overpay for Gimlet. They paid an amount equivalent to all podcast revenue, which is a lot. I looked on Podtrac as a quick gauge for how well Gimlet is doingand Gimlet isn’t in the top ten. Meanwhile, the top ten list is filled with major media companies like NPR, ESPN and even independents like PRX and Wondery. Moreover, between PodcastOne, The Ringer and Radiotopia and huge independents like Joe Rogan and Hardcore History, there are quite a few companies in this space, so buying one producer may not be the edge it portends.

Which is why everyone rightly emphasized this is about the aggregation play on podcasts, emphasizing the acquisition of Anchor. My second worry is “overestimating the effect of originals”. Basically, I see this a lot where every decision from the streaming companies–mostly video–is justified by acquiring new customers. Prestige TV shows like House of Cards? Acquiring customers. Amazon spending at Sundance? Acquiring customers. Kids TV, stand up comedy, nature documentaries, event TV? Customer, customers, customers. The problem is when you add each customer up, well you may have invested too much and overestimated the customer you would acquire.

Frankly, it is a big ask that customers will go to Spotify exclusively for podcasts or even permanently. If there is one podcast exclusively on Spotify, maybe you only listen to it on Spotify. But maybe you skip it because, if you’re like me, you already have too many podcasts in your feed. And maybe their UX isn’t as good as your current app, which is optimized for podcasts, not all music.

For podcast producers, it still may not make sense to go to Spotify exclusively either. If it your podcast is still ad-supported–meaning Spotify isn’t paying you a license fee for it–than exclusivity to Spotify could cripple your ability to build an audience. Launching on one platform immediately limits your monetization potential by artificially shrinking your potential audience. So I have worries.

Other Contenders For Most Important Story of the Week

HBO Changing Launch Days for (some) Series

This had the longest shot to become an actual story of the week. I mean, one premium cable channel-cum-streamer moving some of its shows (a distinction some headlines didn’t convey) isn’t the biggest move on the planet. But it did get me thinking about the value of launch days in general. In some ways, Sundays being the “best” days for cable/premium launches is a “tragedy of the commons” problem in that everyone in prestige from AMC to HBO to Showtime launches on Sunday nights, so no one wins.

Yet, some of the logic behind the move was more likely about competing against yourself if you’re HBO than others. At one point, I watched four Sunday night HBO shows. (Game of Thrones, Silicon Valley, Veep and Last Week Tonight with John Oliver) If they all come out on Sunday, well some were DVR’ed and saved for later. Moreover, for PR purposes, four of those shows demand a recap story on the Slates/Vox/HuffPo’s of the world. If all four air on the same night, they can’t all get on the front page. So that’s two compelling reasons to move the air dates of some shows. (Also, as the NY Times points out, they may have so much content they don’t have a choice.)

I can argue against this, though. Nothing in the broadcast era was more powerful than tune in viewing as people stuck around all Thursday night on NBC. Maybe some of that effect still works, even for a premium channel like HBO. (Though, yeah obviously it is shrinking.) Moreover, claiming a night for when people can expect premium TV makes sense and, according to some stats, Sunday is the most viewed night of TV of the week.

Sum it all up, and I can’t predict if this is a good move or a bad move. What I can say is it isn’t meaningless. Netflix constantly tweaks their product launches, so HBO should too to maximize impact. I’m always for tweaking a model or business to maximize your competitive advantage, and I could see the arguments for this, especially if it helps dominate the PR impact.

Since most of the #MeToo era started before I launched this website, I haven’t written a lot on it, though it definitely has impacted a lot of the business. Often that’s because individual stories don’t really impact the business, and fall into the category of “celebrity news” than business news. This iteration is different and I’d refer you to The Business podcast from last week for why.

There is a difference between refusing to work with someone for future projects and cancelling already signed deals. Cancelling deals could cause lawsuits. Or a studio could choose not to work with someone, but keep paying them. Paying people who have inappropriate conduct on set could cause bad PR coverage and internal moral problems. So lose lose. (Refusing to work with someone results in neither of those outcomes, unless you misjudge the PR angle, a la James Gunn and Disney.) In short, with challenges like Woody Allen, there aren’t any good options. It’s probably a tough case for Amazon to decide, which means the courts will settle it, and as they say bad cases make bad case law.

While I’m talking about The Business podcast, I heard this news again on THe Business this week, and for some reason it stuck with me. I need to think more on this, but I would love to figure out more of the business ramifications of layoffs of this size.

Lots of News with No News

Disney Earnings Report – Streaming will cost money

Since Disney has two different groups of fanboys (Star Wars and Marvel) in addition to a bunch of diehard fans following it–wait, does that include me?–usually the biggest stories involve random drops of trivia. So Disney repeated on their earnings call that they will keep making R-rated movies (which they had already said) and that the theme parks will come in later half of this year. The non-news financial news is that ESPN Plus has 2 million subscribers, which I’d call neither good nor bad. It just is, and we’ll see what it means.

They’re also going to lose money as they transition from sellers to streamers. Hmm.

If I were really cynical–and I am–I’d say that if starting your own streaming company loses lots of money–and we’re now 4 for 4 (Netflix, Disney, Hulu and Seeso, if not more) on data points in that regard, with a “TBD” in Amazon–then maybe we’re all investing our capital inefficiently? Or that there are “bubblish” elements where certain players are overpaying, which causes everyone to lose money, which makes these bad investments? If I were cynical though.

There is no smaller sample size than one.

If you understand that, then all the discussions about why the Super Bowl had low ratings feel a lot more hollow. I’d call them “narrative explanations” as opposed to data-based, because, again, it is a sample size of one. So maybe people were sick of watching the Patriots, or OTT actually showed higher ratings (it didn’t) or football is losing popularity, Or maybe the Chiefs and Saints make the playoffs and the highest ratings in history happen? I don’t know. (I explained the difference between narratives and data when Solo came out and with M&A hype.)

(Also, the TV ratings were US only. From now on, headline/Twitter headlines should include geography when numbers or effect are measured.)

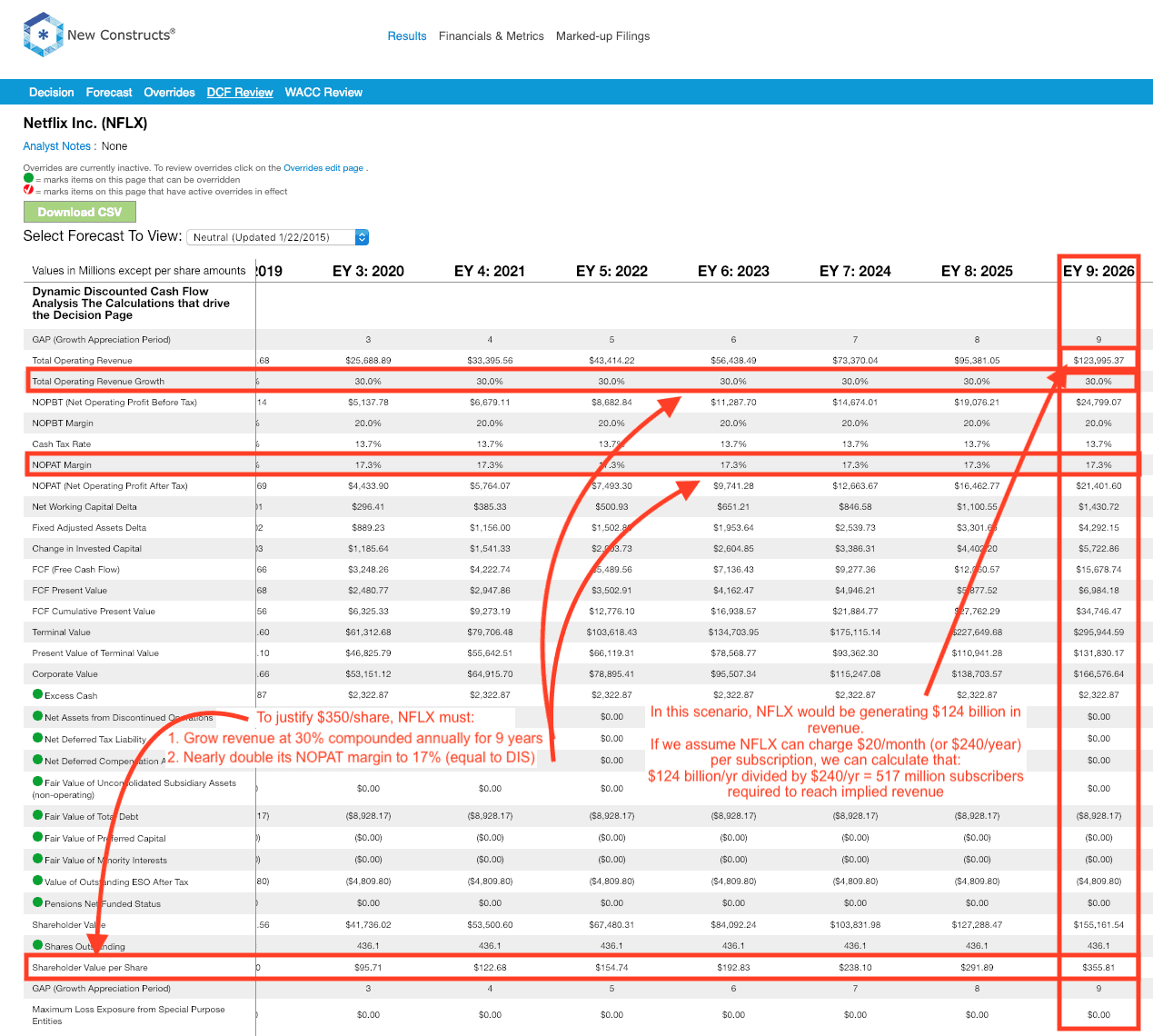

Long Read of the Week – Reality is Closing in On Netflix

Since I haven’t mentioned Netflix yet, I’m required by entertainment journalism bylaws to do so now. Check out the work of New Constructs from after Netflix’s earnings report. I love their writing in general as they apply the type of data-based analysis that is missing often in the discourse. Strategy is numbers, right? Speaking of which, they show their math in this Excel spreadsheet.

{kind=link}