The first thing to know about the streaming wars is that it is really multiple wars simultaneously. One war is between the streamers. They compete fiercely against each other, with Netflix in the lead. (This is by far the most covered battleground.)

If those are the established powers, the upstarts are the free, ad-supported streamers are trying to take territory, er attention/mindspace/viewership, from both. Youtube leads here, but is followed by the hot new crowd of Pluto, Xumi, Tubo, Roku/IMDb Channels, and more.

Yet, those land armies’ power is dwarfed by that of the air forces of the world. Who in many cases set the terms of the streaming wars. And in this analogy, that’s the platforms that deliver the streamers, be they devices or operating systems or other bundlers have just as much, if not more, power. In a moment, a platform could blow up an entire business model, like dropping a nuclear bomb on an opponent’s army.

(The Game of Thrones analogy patented by Dylan Byers also explains this well: streamers are the traditional houses of Westeros, ad-supported streamers are Daenerys and the Dothraki, and the platforms are the White Walkers.)

If you want to understand the scope of Epic Games going to war with Apple, this is it. Epic Game’s army is fighting Apple’s air force, with the expected outcome that Apple nukes Epic’s business.

For those who don’t know, Epic Games (maker of the Fortnite game and Unreal video game engine) tried to implement in-app purchasing outside of Apple’s payments system. This resulted in them being kicked off the Apple app store, lawsuits and countersuits.

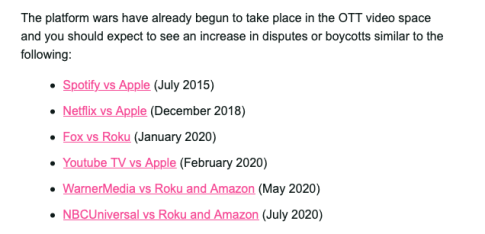

The Fortnite gambit will directly impact the streaming wars. The ability of platforms to dictate terms to the streamers directly hits streamers’ top, bottom and cash flow lines. If Fortnite wins, it is like taking away Apple’s (and Google, Roku and Amazon’s) ability to drop bombs. (Okay, I’ve taken this analogy about as far as it will go.) That’s what I’m going to explore today:

- First, explaining the relationship between aggregators, streamers, bundlers and platforms.

- Second, describing the “maximalist” scenario where platforms are heavily regulated.

- Third, understanding the impact across the three forms of streaming business models:

– Transactions (Pay per usage)

– Subscriptions (Pay a recurring fee for access)

– Advertising (Free, but watch/listen to advertisements)

Putting this In Context

As I wrote last November, the key to understanding the streaming wars is to know that a huge amount of power is vested in what I call “Digital Video Bundlers”, the folks bundling multiple streamers into one experience. Here’s where they are on the map, yellow:

Fortnite would slot in where I put “aggregators”, though that term is more apt for streamers than gamers like Fortnite. Apple is the bundler, since they allow a user the opportunity to play multiple games on one device. Crucially, Fortnite—like many app makers—wants to be more. They want to sell additional things within its game to make more money. Epic Games also wants to set up an entire app store on its own. (Really, Epic Games has dreams of being a bundler as well.)

The conflict stems from those in-app purchases. Since Apple owns the operating system, it wants a piece of any money being exchanged on its platform. When you buy an application, you pay Apple 30% of that price. On some level this makes sense. Apple set up the platform so they should get paid for letting you on the platform.

This is a “platform tax” that Apple charges to have an application on its App Store. And Amazon and Google have similar taxes. (You could call it a “fee”, “rent”, or other term, but I like tax.) A tax for doing business on their platform. Apple says this is the price needed to run its App Store.

That’s what makes the terms of this court case so large. If Fortnite wins, they won’t just change their own terms, but alter the fundamental case law around platforms. The results could impact Apple, Microsoft, Sony, Google, Amazon, Roku and any other platform.

The Maximalist Scenario

That’s the world I want to imagine today. I’m calling this the “maximalist” scenario. It assumes a judge/judges/legislative bodies/regulatory agencies use the Fortnite case to legislate/regulate/litigate maximum concessions from an Apple, Amazon or Google on their platforms. Call this the “worst case” for platforms or the “best case” for streamers, applications and games. Say…

– A 3% cap on fees (or cap on fees up to a given maximum).

– Guaranteed carriage on non-business issues

– No tying disparate business unit negotiations together.

Essentially, in this scenario digital market places like app stores are governed as utilities. The government would be saying, “Since you have de facto monopoly power over app stores, we have to regulate your business to ensure you don’t abuse your power.” I’m not assuming this happens, but exploring the “what if” scenario where it does.

Impact on Transactional Business Models

The impacts on the transactional video-on-demand (TVOD) market would probably be the starkest of any of the business models.

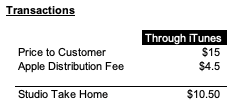

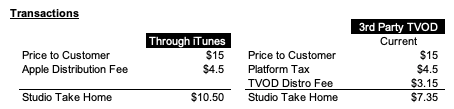

Fundamentally, the platform tax makes any external TVOD business unworkable on any mobile device. The math is fairly simple. If you’re Apple, and you own your own TVOD business in iTunes, your gross margins look like this:

Now compare that to an independent service trying to run a TVOD business on iTunes:

Both the new app and iTunes have to split revenue with the studios. That’s the “TVOD distribution fee” and it’s currently about 30%. The challenge for someone trying to disrupt iTunes on Apple’s OS is that they have to pay that fee AND Apple’s platform tax.

As a result, all the major TVOD players own their own device/platform and there are few competitors. In rough descending order, it’s Apple’s iTunes, Amazon’s Prime Video, Microsoft X-Box/Sony Playstation and Google Play. The reason is simple: if a new entrant tried to offer lower prices, the device owners could always undercut them on price. While making much better margins. (Amazon, in particular, has algorithms that do this already for most of their website.)

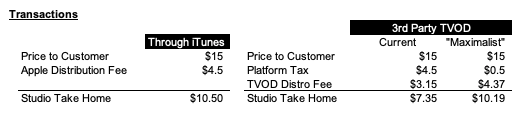

At 3%, the gross margin isn’t enough to fundamentally change the game. (Saving $0.45 on a $15 film doesn’t matter; saving $3 does.) At 3% platform taxes, a TVOD service with an innovative model really could compete with the platforms themselves.

What would happen if the maximalist scenario happened? Well, you’d see a some new TVOD services. I’m not sure how many and how quickly, but “TVOD” would go from an unworkable biz model to a viable one overnight. The barriers to entry would have evaporated, and inevitably that means more new entrants.

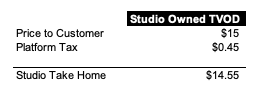

The traditional studios would have to most to gain from tearing down these walls. Just look at the math:

If Disney+ didn’t have to pay a 30% tax (and I bet their price is lower since they’re so important to Apple, but not that much lower), then they’d likely keep all their movies exclusive to their own new TVOD platform. Disney+ is already flirting with this idea. You know Comcast is chomping at the TVOD bit, so if the fees came down Peacock would likely add TVOD to the mix too. The other studios could partner on another movie service (again) or go their own way.

Studios owning their own TVOD would present new antitrust issues, but it’s likely the result in this maximalist scenario.

Impact on Subscription Business Models

While TVOD has a hypothetical game changer, the change to subscriptions wouldn’t be as dramatic, but would happen even faster. Mainly because the impact of the platform tax on monthly subscriptions multiplies by every month. And maybe years.

The 30% fee that Apple wants to collect via in-app payments isn’t just for one time fees, but also recurring subscriptions. 30% of a monthly subscription drastically hurts margins.

That’s $126 dollars per customer. That really adds up! Hence why Netflix, Spotify and a growing crowd don’t let Netflix handle subscription payments. (To be fair, many streamers also offer bounties to device companies for signing up customers in the first place. So this math is simplified for demonstration purposes.) Kirby Grines captured the fights over platform taxes in just the last few years recently in his newsletter:

I see three key impacts to the subscription landscape if this happened.

First, in-app subscriptions would be come the norm. There is a big gap between 3% and 30% (or even 3% and 10%). Even Apple doesn’t like that Netflix forces consumers off its platform to sign up for Netflix. That’s a bad user experience. But Netflix can’t afford at its cash burn to give Apple 10% of its subscription revenue. (I assume Apple and Netflix have negotiated lower rates due to Netflix’s importance.)

Indeed, the list is much longer for major companies that have not caved to Apple in streaming (Netflix, Disney+, HBO Max, Spotify) than companies that pay the passthrough (Amazon). The Amazon example is particularly rich, because the main reason the two tech giants came to an accord is because they were both threatening each other’s businesses on a variety of fronts. Thus they had was more room to make a deal (and each has the cash flow to support losses in minor businesses).

The second impact would be to lower monthly prices across the board. It’s a rule of economics that lower prices drive higher adoption. If platform taxes became negligible, the streamers could either pocket the extra cash or they’d lower prices.

My gut is they’d opt for the latter. We’ve already seen Disney and HBO Max offer fantastic deals to customers to sign up directly via their websites. Why? To avoid the platform tax. And often the deal price is about 20-30% off the regular price…or the exact amount of the tax. Meaning the streamers seem willing to sacrifice some revenue so they can add more eyeballs. And even if we didn’t see prices decrease, we’d see them at least stay flat.

The third impact wouldn’t be as good for customers. Once platforms are less lucrative at generating recurring revenue via taxes, we’d see prices for devices slowly rise. Roku and Amazon’s explicit business model was to sell devices at cost (or in Amazon’s case, potentially at big losses) and then use the market power to demand rents later. If that business model disappears, consumers would have to pay actual costs when they buy devices.

Impact on Advertising Business Model

Advertising would probably see the smallest amount of changes, but notably, the power of the big tech platforms is partly because they’re trying to collect even in application advertising. Beneath the bundling issues, both Peacock and HBO Max have dreams to launch ad-supported services. And Roku has explicitly told NBC they want to sell some ad-inventory against their service. Amazon has made similar claims.

If Fortnite wins the day, it’s hard how to see that mandating payments for access to a service doesn’t count as tying services or leveraging size. (Since both Roku and Amazon are 25% of the streaming video market, that’s a pretty clear case for using size to force compliance.) They’d be tying a separate business (selling ads) to operating a market place.

Thus, we’d probably see the rise in ad-supported services continue or accelerate, since the companies wouldn’t have to worry about giving advertising time in their applications. Of the three models, though, this is the realm I’m the least confident in what would happen.

How Likely Is This Scenario?

Not very.

The current business climate can best be described as very pro-business/big business friendly. While we’ve probably passed the “high watermark” in business friendly administrations—potentially the Obama administration, if only because they barely used the Justice Department for antitrust action, and even the Bill Barr DoJ will bring a suit against Google—future governments will still defer to big business more often than not.

The likely outcome of “Fortnite versus Apple” is somewhere between where we are now and the “maximalist” scenario. In other words, the maximalist scenario is the “5th percentile” outcome, meaning 1 out of 20 times it doesn’t happen. It’s the worst case outcome. But the current status quo feels unlikely to stay the exact same.

As I mentioned a few weeks back, monitoring how the US government treats antitrust is a key forecasting variable for me. If a new Biden administration is serious about consolidation, it could have huge ramifications for technology and entertainment. And Fortnite is just starting to make that an issue.